Simplify Recurring ACH Payment Processing with AI

Key Takeaways

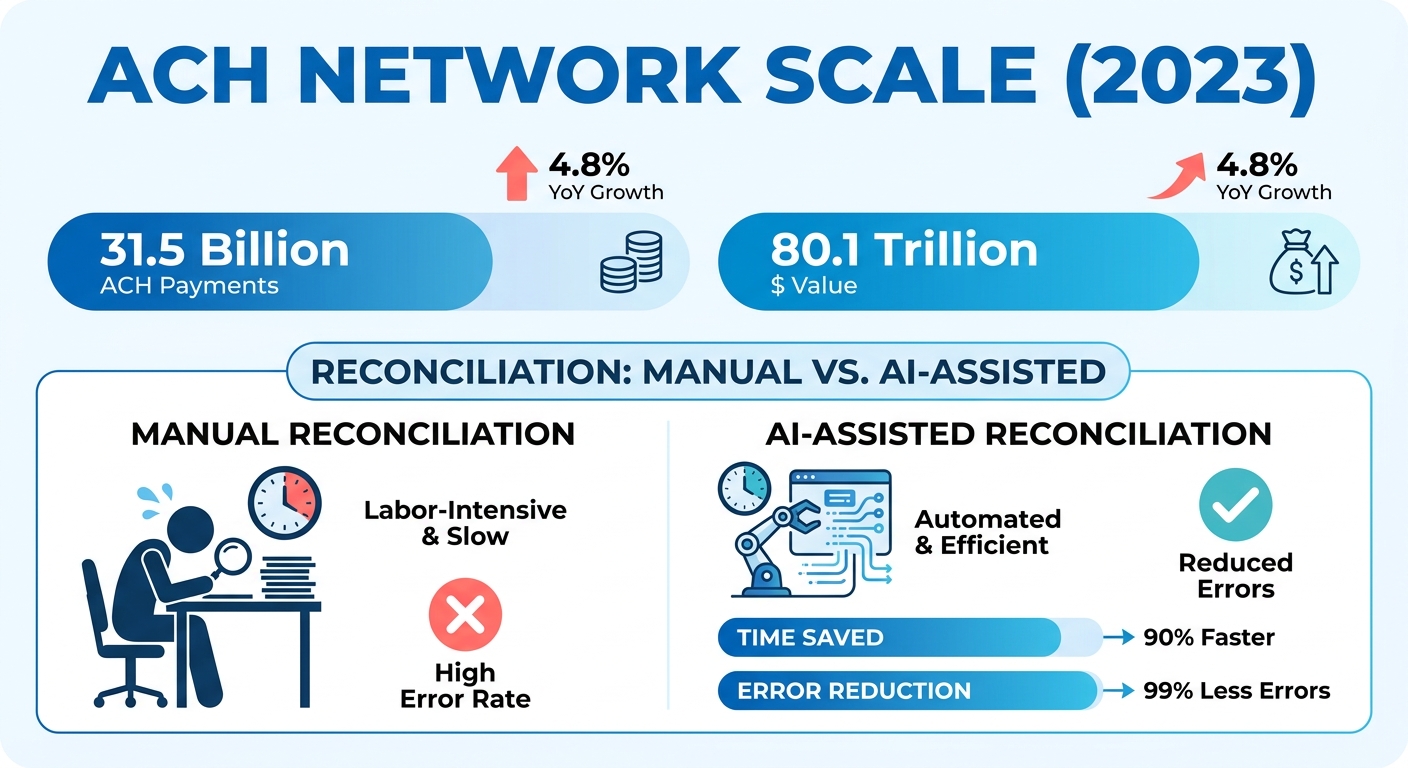

- The ACH network moved nearly 31.5 billion payments worth $80.1 trillion in 2023, up 4.8% in volume year over year.

- Standard ACH settles in 1 to 3 business days. Some processors quote 3 to 5. Either way, finance teams sit blind on payments in the meantime.

- Batch processing keeps ACH cheap but strips out remittance detail, so a lump deposit rarely maps cleanly to individual invoices.

- The real bottleneck isn’t collection. It’s reconciliation, connecting each deposit back to the right invoice, and that still happens largely by hand.

- Manual matching breeds errors that inflate AR, hide failed payments, and quietly push up days sales outstanding.

- AI matches incoming ACH payments to open invoices the moment the data lands, finishing reconciliation in minutes instead of days.

- Natural language processing reads the messy remittance data a human would otherwise have to decode by hand from raw bank files.

Why recurring ACH still trips up finance teams

Pulling a recurring debit is easy. Knowing where the money landed is not.

As transaction volumes climb, the old back-office workflows can’t keep up. For subscription businesses, the scale is the problem: thousands of identical charges every cycle, and reconciliation still leaning on manual matching.

The core issue is visibility. Initiating a debit is straightforward. Matching each settled deposit back to its open invoice fast enough to keep an accurate cash position is the part that breaks.

What’s actually broken in standard ACH

It starts with the clearing window. During those multi-day settlement periods, finance teams work half-blind, unable to confirm which accounts cleared and which subscriptions are still live.

Then there’s the structure of bulk clearing, which strips out the granular remittance detail. When a dozen customer payments collapse into one lump-sum deposit, your AR team is back to parsing raw bank files to figure out who paid what.

That hands-on parsing is where the errors creep in. Misallocated funds hide delinquent accounts, stall collections follow-ups, and skew the metrics you actually report on, like outstanding balances.

How AI fixes real-time cash application

Automation drops an intelligent parsing engine straight into the payment stream. By reading unstructured text and picking up contextual clues in bank files, the software resolves most discrepancies without a human looking at them.

That means the ledger updates continuously. Routing logic flags anomalies for fast resolution, and predictive models read historical clearing patterns to anticipate settlement issues before they bite. The subscription ledger reflects your real cash position much sooner.

Speed up that cycle and your working capital metrics improve directly. When cash application happens alongside settlement, treasury can forecast liquidity with far more precision. One mid-sized company that automated its high-volume disbursement workflow cut its admin processing cycle in half and killed off manual entry errors in the process.

Who gets the most out of it

SaaS and subscription businesses, hands down. They run high volumes of identical recurring charges, so automated matching pays off every single billing cycle. ACH fees stay low too, often under 1% or a flat $0.20 to $1.50 per transaction, against 2.5% to 3.5% on cards.

The retention case is real. One subscription service that switched to recurring ACH saw a 30% lift in customer retention along with a sharp drop in admin overhead.

Here’s how the common approaches stack up:

| Method | Settlement Time | Cost per Transaction | Recurring Fit | Auto-Reconciliation | Admin Workload |

|---|---|---|---|---|---|

| Paper checks | 5+ days | High (handling) | Poor | None | Heavy |

| Credit cards | 1-2 days | 2.5%-3.5% | Good | Partial | Moderate |

| Standard ACH | 1-3 days | $0.20-$1.50 | Strong | Manual | Moderate |

| Same-day ACH | Hours | ACH + fee | Strong | Manual | Moderate |

| AI-enhanced ACH | 1-3 days | $0.20-$1.50 | Strong | Automatic | Light |

ACH already wins on cost for recurring billing. AI-driven matching is what turns it into a real-time view of your cash. For a deeper look at structuring these flows, see this recurring payments guide.

AI-driven cash application and reconciliation

Modern cash application platforms reconcile incoming transfers against outstanding balances even when the metadata is fragmented. For contract-billing cycles, that turns reconciliation into a continuous background process. A settlement notification comes in, the system identifies the payer, and the ledger updates itself.

It works especially well on recurring revenue. When the same amounts hit on a predictable schedule, the model recognizes the cadence fast and clears matches with high confidence.

How AI matches payments to invoices

The matching engine runs on ingestion and parsing. Semantic analysis pulls unstructured text from wherever it lives, email notifications, PDF remittance advices, bank memo fields, and turns it into structured data. That gets cross-referenced against open invoices using fuzzy logic, so minor spelling variations and truncated names don’t break the match.

The standout part is matching with incomplete data. A customer sends an ACH payment with no invoice number, a truncated reference, or a lump sum covering three months. Good cash application tools reconcile it to the right invoices anyway, using past payment behavior to fill the gaps.

Close the gap between settlement and posting and you sidestep the classic unapplied-cash trap. No funds parked in suspense accounts while an analyst plays detective. Payments get recognized immediately, and the aging AR balance stays honest.

What you actually get out of it

The wins center on efficiency and scale. Automate the ingestion pipeline and your finance team absorbs higher volumes without adding heads, with savings compounding across thousands of billing cycles.

Real deployments back this up. One company recovered $33.4 million** in deductions with a 34-day resolution time, well ahead of its industry's 90-day average. Another cut **$2.5 million in financial services costs while handling more volume. A third reported a 75% jump in revenue recognition productivity after automating its close and reconciliation.

There’s a 24/7 angle too. Instant payments can verify and clear in milliseconds, and the newer agentic AI systems detect a return, update payment instructions, and resubmit on their own. Nobody needs to be at a desk for the workflow to keep moving.

What to plan for before you trust it

Two big hurdles: data quality and integration. AI matching is only as good as the remittance and invoice data feeding it. Dirty records or inconsistent customer naming will throw exceptions that still need a human.

Integration is the second gate. The best cash application tools connect natively with major ERP systems, so settlements flow straight into your ledger. If your billing data is scattered across disconnected systems, you’ll burn setup time wiring those feeds together before the AI earns its keep.

Start with your recurring ACH book. That’s where the patterns are cleanest and match rates highest. Prove the model there, clean up the exceptions it surfaces, then expand to one-off and partial payments once the foundation holds. That sequencing buys you faster reconciliation and lower DSO without betting the whole close on day one.

Timing payments and cash flow with AI

Liquidity comes down to tight alignment between when funds settle and when the ledger updates. Speed up verification of incoming transfers and treasury gets immediate clarity on available cash, instead of waiting on an end-of-day batch.

The volume behind this is climbing fast. The ACH Network processed 35.2 billion payments worth $93 trillion last year, with B2B volume up 9.9% year over year. Every one of those recurring subscription debits is a matching decision, and AI makes it instantly rather than queuing it for a human.

How AI improves payment timing and cash flow

Predictive analytics forecast settlement timelines and flag bottlenecks before they hit liquidity. By analyzing historical clearing speeds across different banks, the system helps treasury project cash availability more accurately.

Autonomous workflows protect revenue. When a transaction fails on something temporary like insufficient funds, automated retry logic reschedules the resubmission during a better window. That proactive recovery keeps subscribers in service and cuts involuntary churn, no manual chase from collections required.

For contract-based billing, this continuous reconciliation keeps accounts in good standing. Rather than manually verifying payments before provisioning or renewing, the system automates status updates and smooths the whole customer lifecycle.

Where the cash flow gains show up

Faster collection, lower cost, less manual work. Real deployments make the scale concrete.

- Lower financing cost: an equipment manufacturer’s treasury team captured $1.3 million in annual interest savings by tightening cash timing.

- Shorter close: a software company compressed its monthly close from eight days to three once auto-matching cleared the bulk of incoming payments without review.

- Fewer exceptions: a subscription provider lifted its straight-through match rate to 92%, leaving only a thin slice of deposits for an analyst to touch.

Smaller shops see it too. A regional services firm that moved recurring debits onto AI-driven ACH cut its days-to-cash by roughly a week. Less admin friction, faster liquidity. The link is that direct.

What to plan for before you trust it

These gains depend on data standardization. Across multiple subsidiaries or diverse customer segments, inconsistent naming conventions will choke automated matching. Lock in standardized customer identifiers across every billing channel before you deploy, and your match rates hold up.

Your system architecture matters for timing, too. Traditional batch file transfers (SFTP) introduce periodic delays. Modern API-based integrations sync data instantly between your payment gateway and ledger, so your cash position stays current in real time.

Picking an ACH provider and AI layer that fit

Picking a provider is about more than transaction fees. The reconciliation engine is what matters most. For high-volume subscription models, a low per-transaction rate means little if manual matching costs stay high. You want strong clearing plus an intelligent automation layer on top.

Most providers fall into two camps. Bank-direct processors handle the transfer cheaply but leave reconciliation to you. Software platforms wrap the transfer in automation, and the strongest ones add AI-powered cash application that reads remittance data and posts matches with nobody in the loop.

What to look for in an ACH provider

Prioritize tiered volume pricing and solid developer tools. As your subscriber base grows, a partner that drops your per-item cost at volume thresholds meaningfully improves unit economics. Look for thorough API documentation too, since it makes custom workflows far less painful.

Settlement speed is the second filter. Standard ACH runs 1 to 3 business days, with Same Day ACH available for an added fee and a $1 million per-transaction cap. If your cash flow leans on fast clearing, confirm the provider supports Same Day before you sign.

Security rounds it out. ACH carries a remarkably low fraud rate, around $0.08 for every $10,000 in transactions. Account validation against large reference databases pushes that even lower and lifts approval rates.

How the AI layer changes the call

An integrated intelligence layer shifts the focus from moving funds to automating the whole workflow. Embed matching directly in the transaction lifecycle and you can automate ledger postings the moment settlement confirms, cutting the time accounts stay open.

The market’s moving this way fast. Paper checks are now just 25% of B2B payment volume, down from 81% in 2004, and three-quarters of organizations still cutting checks blame manual processing inefficiency. AI-driven ACH is the obvious replacement.

Ask whether the provider supports automated recovery for returned transactions. Some workflows recover up to 60% of missed payments by retrying failed debits on a smart schedule. For subscription revenue, that directly protects your monthly recurring base.

How to choose and roll it out

Run a short, ordered process so you don’t buy a tool your stack can’t use.

- Map your volume and ticket size. High invoice values favor flat-fee ACH; confirm the pricing model fits.

- Test the matching engine. Feed it real remittance data, including the messy entries, and measure auto-match rates.

- Verify ERP and accounting integration. Native connections to systems like SAP and Oracle prevent duplicate data entry.

- Check settlement and recovery options. Confirm Same Day ACH and automated retry for returns.

- Pilot before full rollout. Run one customer segment, track DSO movement, then scale.

The payoff compounds at scale. Finance teams that automate cash application usually move staff off manual posting and onto exception handling and collections, where judgment actually adds value. A mid-market biller processing thousands of invoices a month can absorb subscriber growth without adding headcount. Match that against your own recurring billing and the provider choice gets a lot clearer.

Implementation checklist for AI-enhanced ACH

A phased rollout beats a system-wide cutover. Connect data streams methodically, validate matching accuracy as you go, and you transition without blowing up daily operations.

Prerequisites before you start

Before any AI touches your ACH flow, lock down the inputs. The model can only match what it can read, so clean data isn’t optional.

- Bank account details on file: institution name, account type, ABA routing number, and account number for each recurring payer.

- Customer authorization: every ACH debit needs documented authorization specifying amount and schedule, compliant with Nacha rules.

- ERP or accounting integration: confirm your system connects to QuickBooks, Xero, NetSuite, or wherever your open invoices live.

- Clean remittance data: messy or missing remittance is the single biggest reason matches fail.

Skip the data cleanup and you’ll fight false matches for months. The AI inherits whatever garbage your records already hold.

Step by step

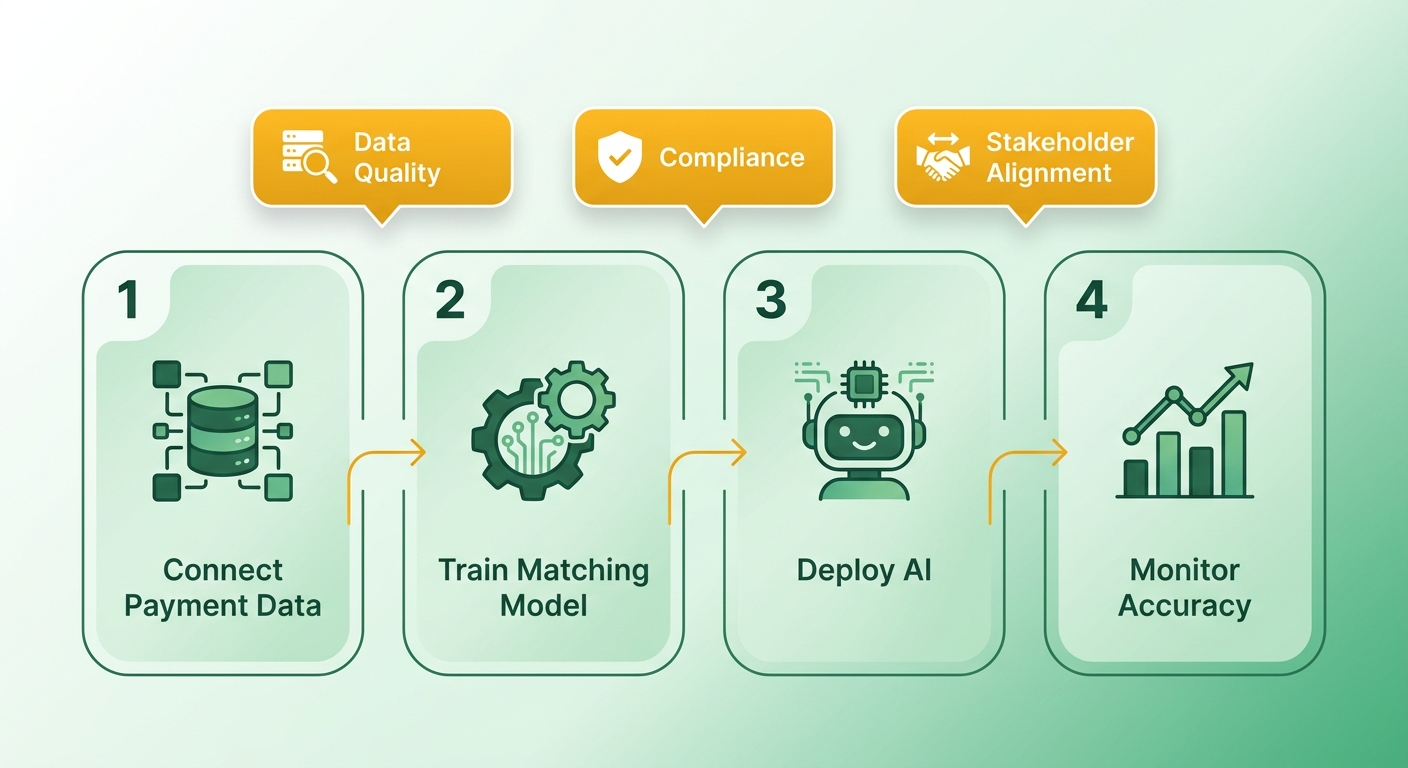

Four stages: connect, train, validate, automate. Each one builds confidence before you hand more decisions to the model.

1. Connect your payment and invoice sources. Link your bank feed and your ERP so the AI sees incoming deposits and open invoices in one place. Because of standard clearing windows, configure it to monitor pending settlements and match them as they finalize.

2. Train the model on your recurring patterns. Feed it historical transaction logs. Over time, the algorithm learns the recurring payment sizes and cadences tied to specific accounts, setting a baseline for match confidence.

3. Validate with an approval workflow. Don’t go fully autonomous on day one. Run a human-in-the-loop step where staff confirm or correct matches. Every correction trains the model to do better next time.

4. Automate exception handling. Once accuracy holds, switch on automated resolution. Configure the system to flag returned items, notify account managers, or trigger pre-defined retry schedules without manual intervention.

What results to expect

Faster reconciliation, fewer late payments, and a measurable drop in admin work. When the AI clears predictable recurring deposits on its own, your team stops matching payments by hand and your cash flow gets easier to forecast.

For maintenance, keep retraining. As you manually edit matches, the system gets sharper and matches better next time. Run regular audits to stay compliant with Nacha rules and catch drift early.

One caveat: if your billing is low-volume or wildly irregular, the model has little pattern to learn from. AI cash application shines on predictable recurring revenue. For one-off project invoices with no cadence, the payoff is thinner.

Frequently Asked Questions

1. What happens when a recurring ACH payment fails or gets returned?

Returned ACH payments trigger standard Nacha return codes like R01 (insufficient funds) or R02 (account closed), which are typically communicated by the bank within 48 hours. Automated systems handle these by categorizing the failure code and executing pre-configured recovery rules. For example, soft declines like temporary insufficient funds can be queued for automatic re-presentation at a later date, helping recover a significant portion of outstanding revenue without manual collections outreach.

2. Is ACH safer than accepting credit cards for recurring billing?

Yes, bank-to-bank transfers generally experience significantly lower fraud rates compared to card networks. To mitigate risk, businesses utilize real-time bank account verification services to confirm account status and ownership before initiating transactions. The primary trade-off is authorization speed; unlike credit cards, which approve or decline instantly, bank transfers require waiting for the standard clearing cycle to confirm successful settlement.

3. Do I need customer authorization before debiting recurring ACH payments?

Yes, obtaining explicit consent is a fundamental requirement under Nacha operating guidelines. This mandate protects both parties by establishing clear terms for the frequency and amount of the debits. Businesses must securely store these agreements and provide customers with advance notice of any changes to the billing schedule to prevent unauthorized debit disputes.

4. Will AI cash application work if my business has irregular or low billing volume?

While automated matching tools can still parse individual bank files, the return on investment is lower for businesses with highly customized, sporadic invoicing. The machine learning models rely on historical consistency to achieve high-confidence auto-match rates. If every transaction is unique in size, timing, and customer profile, the system will generate more exceptions requiring manual review.

5. How is Same Day ACH different from standard ACH for subscriptions?

The primary difference lies in processing frequency and cost. Standard processing relies on overnight batch cycles, whereas the Same Day option utilizes multiple daily settlement windows to move funds within the same business day. Because Same Day transactions incur premium processing surcharges and are subject to network-imposed transaction limits, standard clearing is typically preferred for predictable, non-urgent subscription renewals.

6. Which accounting systems should an AI ACH tool integrate with before I commit?

Your chosen tool must integrate directly with your primary system of record. Seamless data synchronization ensures that when a payment is matched, the corresponding invoice is marked as paid automatically. Look for platforms that offer pre-built connectors for your specific accounting software or ERP, which avoids the need for custom API development and prevents manual data entry errors.

7. How do I keep AI match accuracy from drifting over time?

Long-term accuracy is maintained by establishing a feedback loop. When exception handlers manually resolve a mismatched payment, the system analyzes the correction to refine its matching rules for future cycles. Additionally, conducting periodic quality assurance reviews helps identify systemic changes in customer payment behavior, ensuring the algorithm remains aligned with your evolving billing patterns.