Recurring ACH vs Credit Cards for Timely Payments

Key Takeaways

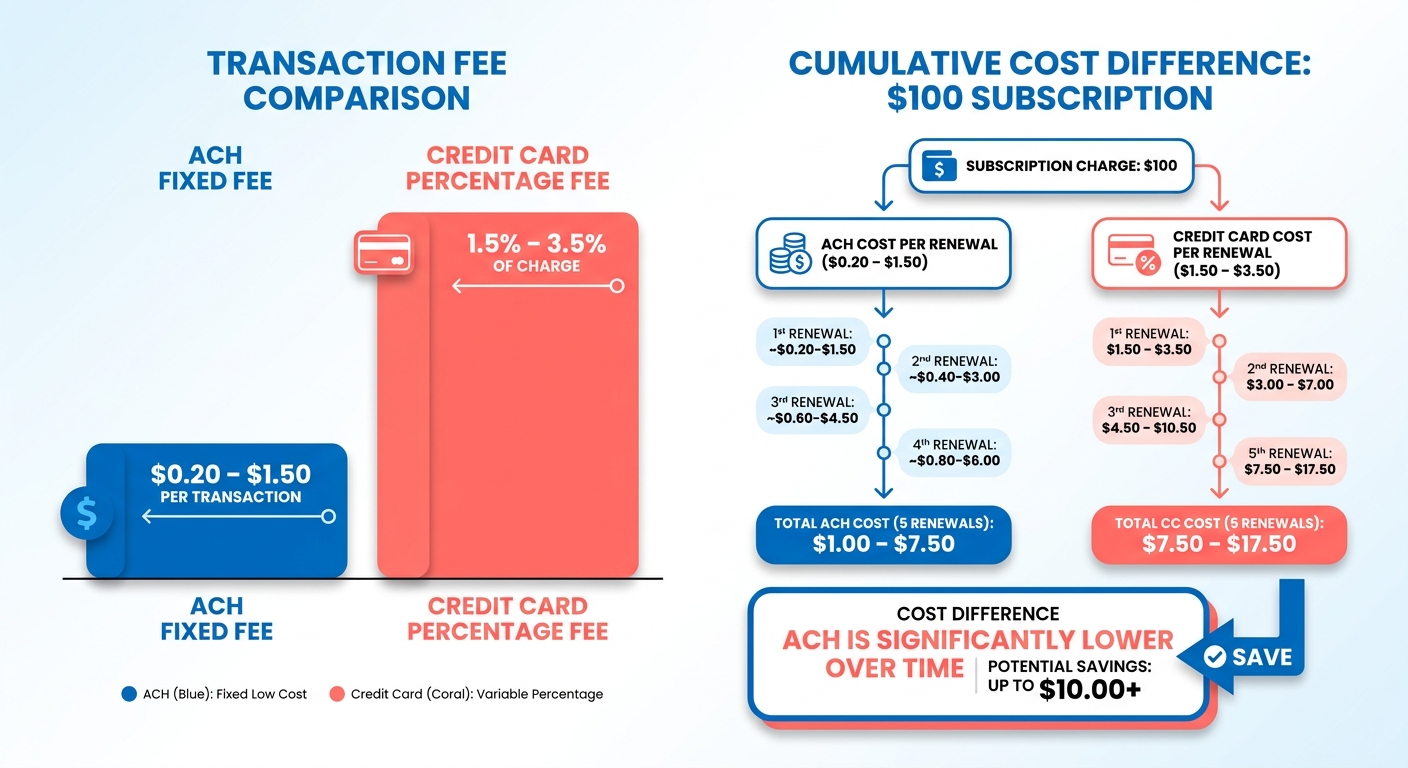

- ACH runs $0.20 to $1.50 flat per transaction. Credit cards take 1.5% to 3.5% of every charge.

- A mid-sized business pushing 5,000 orders a month at $100 each could save around $13,750 monthly by moving renewals from cards to ACH.

- Card costs scale with your price point, so ACH wins big on high-ticket and predictable subscription billing.

- Bank account details stay put for years. Cards expire and get reissued, which is what quietly kills renewals.

- Cards are faster: instant authorization, one-to-two-day funding. ACH takes one to three business days.

- Cards guarantee funds and fit signups and one-off purchases. ACH carries no such guarantee.

- Chargeback risk is lower on ACH, which adds a little extra protection for recurring revenue.

ACH vs. Credit Cards: Where Each One Actually Wins

If you’re a SaaS founder billing the same customers month after month, the tradeoff is simple. ACH wins on cost and retention. Cards win on speed and convenience. ACH fees land between $0.20 and $1.50 per transaction. Card processing eats 1.5% to 3.5% of every charge. On a $100 subscription that gap looks small. Multiply it across thousands of renewals and it stops being small.

Which one costs less for recurring billing?

ACH costs less. Full stop. Card fees are percentage-based, so they climb with your price point. ACH stays mostly flat. That’s why high-ticket and predictable subscriptions favor it. One mid-sized business running 5,000 orders averaging $100 could save up to $13,750 a month just by shifting renewals off cards.

But fees aren’t the whole story. Churn matters as much. Cards expire, get reissued, hit limits, and when a renewal silently fails you get involuntary churn. Bank account details don’t do that. They stay stable for years. That reliability is the quieter reason ACH protects recurring revenue, and it’s worth more than the fee savings alone suggest.

| Feature | Recurring ACH | Credit Cards |

|---|---|---|

| Transaction fee | $0.20–$1.50 flat | 1.5%–3.5% + per-txn fee |

| Settlement time | 1–3 business days | Instant auth, 1–2 day funding |

| Involuntary churn risk | Low (stable bank details) | Higher (expiry, reissue) |

| Chargeback risk | Lower | Higher |

| Funds guaranteed | No | Yes |

| Best for | Ongoing renewals | Initial signup, one-off |

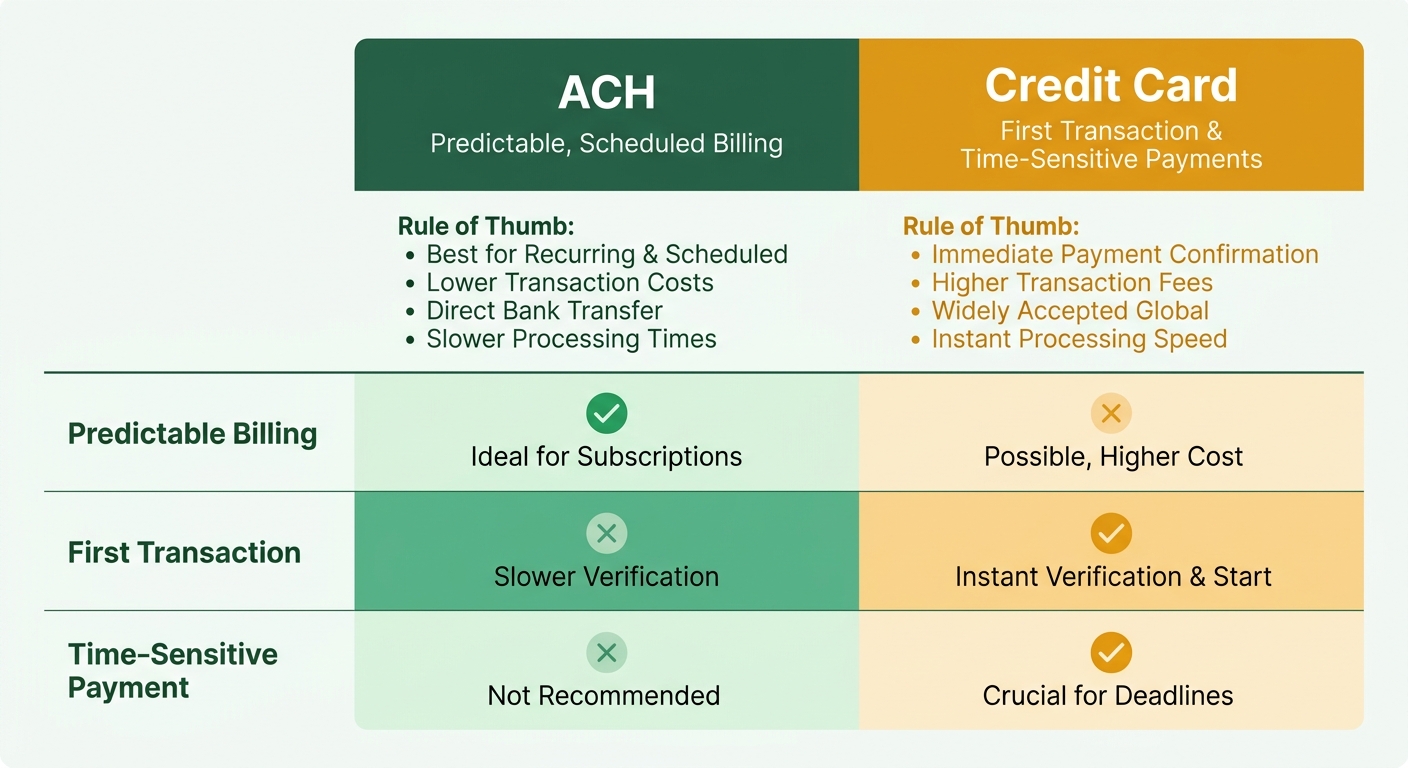

When cards are the right call

Use cards for the first transaction and for customers who won’t hand over bank details. Cards authorize in real time, so you get instant confirmation a new signup actually paid. That immediate feedback lifts checkout completion and starts the service without a one-to-three-day wait.

Cards also carry rewards, and customers notice. Credit cards passed cash to become 32% of all consumer payments recently, and 42% of adults name cash back as their top reason for opening one. For B2C subscriptions, refusing cards at signup costs you conversions you didn’t need to lose.

The smart play is hybrid. Catch customers on a card at signup for speed, then nudge them toward ACH for ongoing billing to cut fees and steady the revenue. Businesses running that split report lower processing costs and higher lifetime value.

How Blixo runs both rails

Blixo handles ACH and card billing from one system, so you stop reconciling two payment streams by hand. It automates recurring charges, retries failed payments, and matches settled funds to invoices on its own. That kills the manual cash-application work that drains finance teams.

On timing, it tracks both the instant card authorization and the multi-day ACH funding window, then reconciles each as the money lands. Failed ACH returns and expired-card declines show up in one place instead of two.

For a founder, the payoff is concrete. Offer cards where they convert, default renewals to cheaper ACH, and let automation handle the dunning and reconciliation that eat hours every cycle. Fee load drops, fewer renewals fail silently, and the books stay clean without spreadsheet wrangling.

Picking the Rail That Actually Fits Your Business

The right method comes down to three things: your industry, your size, and how predictable your cash flow has to be. SaaS founders billing the same customers every month should default to ACH for the recurring charge and keep cards for the moments speed wins the sale. That split keeps costs low without bleeding signups.

The rule of thumb most payment people land on: use ACH for predictable, scheduled billing. Use cards for the first transaction and any time-sensitive payment where instant authorization closes the deal.

Which rail fits your industry?

Match the rail to the use case, not the reverse. B2B services and SaaS should run recurring invoices on ACH to keep fees flat. E-commerce and mobile-first products lean on cards because instant authorization improves checkout completion. The pattern holds across sectors:

| Industry | Best for Recurring | Best for One-Off |

|---|---|---|

| B2B / SaaS | ACH for subscriptions | Cards for international or first-time invoices |

| Property / rent | ACH for monthly dues | Cards for move-in fees |

| Healthcare / education | ACH for payment plans, tuition | Cards for co-pays, incidentals |

| Government / utilities | ACH for scheduled bill-pay | Cards for last-minute payments |

Checkout friction is what you pay for getting the rail wrong. Roughly 70% of online carts get abandoned, and a slow or unfamiliar payment step is one of the top reasons buyers walk. Forcing every new customer onto ACH at signup adds steps exactly when you can least afford them. Let first-timers start on the rail they already trust, then move them later.

How size and cash flow shape the choice

Smaller teams chasing growth should optimize for conversion first, then migrate paying customers to cheaper rails. Larger operations with stable, high-volume billing benefit most from ACH because the savings compound across thousands of renewals. Your cash flow predictability is the deciding factor.

The proven move is mixed: collect the initial signup on a card, then nudge customers to ACH for ongoing billing. It lowers fees and lifts lifetime value, because bank details stay stable for years while cards expire and trigger involuntary churn.

ACH speed has caught up enough to support this. Around 80% of ACH payments settle in one banking day or less, and the network moved 8.6 billion transfers in 2024. That reliability makes ACH a genuine fit for “set it and forget it” subscriptions, not just back-office payroll.

Where Blixo fits your stack

Blixo lets you run both rails from one system instead of stitching together separate tools. It automates recurring ACH and card collection, retries failed charges, and reconciles payments without spreadsheet work. That automation is where the fee savings and churn reduction actually land.

A few things worth setting up cleanly:

- Run both rails side by side during any transition so no payment slips through

- Default new signups to cards, then offer a one-click switch to ACH

- Automate retries and dunning to recover failed payments before they become churn

- Track payment mix and failure rates monthly to see where each rail performs

The goal isn’t picking one rail forever. It’s routing each payment to the cheapest reliable option and letting automation handle the reconciliation you used to do by hand.

Blixo: Both Rails, One System

Getting paid on time comes down to two jobs: automating the charge and reconciling it without manual work. That’s the gap we built our SaaS to close. Whether you run renewals on ACH or cards, we handle the invoicing, the auto-charge, and the matching, so your team stops chasing payments and starts forecasting revenue.

What we do for recurring billing

We automate the full invoice-to-cash cycle for both ACH eChecks and credit cards. Set up a recurring invoice once, and it auto-sends and auto-charges using each customer’s saved payment method. AutoPay handles the charge. Our Cash Application AI matches the incoming payment back to the right invoice, so reconciliation happens on its own.

The retention piece matters most for subscription founders. Cards expire and fail. Our Account Updater refreshes expired or renewed cards automatically, and Retention AI works to head off declined-payment churn before it hits your MRR. That’s the churn half of the ACH-vs-cards decision, solved in software instead of spreadsheets.

For the charges you move to ACH, we accept direct debit with instant verification, keeping fees flat while the same matching engine reconciles every deposit.

How it compares on setup and cost

Here’s where we land against the manual approach most teams start with, plus a typical processor that only handles the charge:

| Factor | Blixo | Card-only processor | Manual / spreadsheet |

|---|---|---|---|

| Payment methods | ACH, cards, checks, wire | Cards (some ACH) | Whatever you bill |

| Reconciliation | Automatic (Cash App AI) | Manual export | Fully manual |

| Failed-card recovery | Account Updater + Retention AI | Basic retries | None |

| Setup effort | Low (hours, no code) | Medium | Ongoing |

| Customer self-service | Branded portal | Limited | None |

| Starting price | $49.99/mo (Team) | Per-transaction fees | Staff time |

Pricing is $49.99/mo for Team and $99.99/mo for Business, both billed yearly, with unlimited customers and invoices. Enterprise is custom for volume discounts. Reviewers consistently flag setup as fast and intuitive, which matches what we hear from agencies and service businesses onboarding without a developer.

Where it fits best

We fit best for B2B SaaS and service businesses billing the same customers on a schedule. If your pain is messy cash application, slow collections, or a billing system that feels clunky, that’s the core of what we replace. Automated collections run reminders by email, SMS, phone, and letter, so delinquent accounts get chased without your team lifting a finger.

The branded customer portal lets clients batch-pay open invoices, swap payment methods, and download statements themselves. That cuts the back-and-forth that delays payment.

When to skip us: if you bill purely one-off consumer transactions with no recurring component, a simple card processor is enough. Our strength is recurring billing and AR automation, so a single-charge storefront won’t touch most of what we offer. For anyone running subscriptions across ACH and cards, the value is in never reconciling a payment by hand again.

Frequently Asked Questions

1. Can customers reverse an ACH payment the way they file a credit card chargeback?

ACH payments can be reversed, but the rules differ sharply from cards. Under NACHA rules, consumers typically get 60 days to dispute an unauthorized debit, while business accounts get just two business days. This much shorter B2B window is a key reason ACH carries lower chargeback risk overall.

2. Does ACH work for international customers?

ACH operates only within the United States, moving funds between US bank accounts. International customers cannot use it, which is why cards remain the practical option for cross-border invoices. For overseas recurring billing, you will need credit cards, wire transfers, or regional rails like SEPA in Europe.

3. What happens when a recurring ACH payment is returned?

A returned ACH payment generates a return code, most often R01 for insufficient funds. You typically pay a return fee of $2 to $5, and the funds claw back from your account. Automated retry and dunning logic reattempts the charge on a schedule before the failure turns into involuntary churn.

4. Can I add a surcharge to cover credit card processing fees?

Credit card surcharging is legal in most US states but capped at your actual processing cost, usually around 3 percent, and prohibited in a few states. Surcharging cards while keeping ACH free is a common, compliant tactic to steer recurring customers toward the cheaper bank-debit rail.

5. How do I move existing card customers over to ACH?

Make ACH the default at renewal and offer a one-click switch rather than a manual opt-in. Some businesses add a small card surcharge or a modest ACH discount as incentive. A branded self-service portal, like Blixo provides, lets customers swap payment methods themselves without back-and-forth emails.

6. Is storing customer bank details for ACH actually secure?

ACH security relies on bank-grade encryption and tokenization, so platforms store a token instead of raw account numbers. NACHA mandates data-protection standards for anyone processing over 2 million ACH payments yearly. Reputable providers verify accounts instantly and never expose full routing or account numbers during recurring charges.